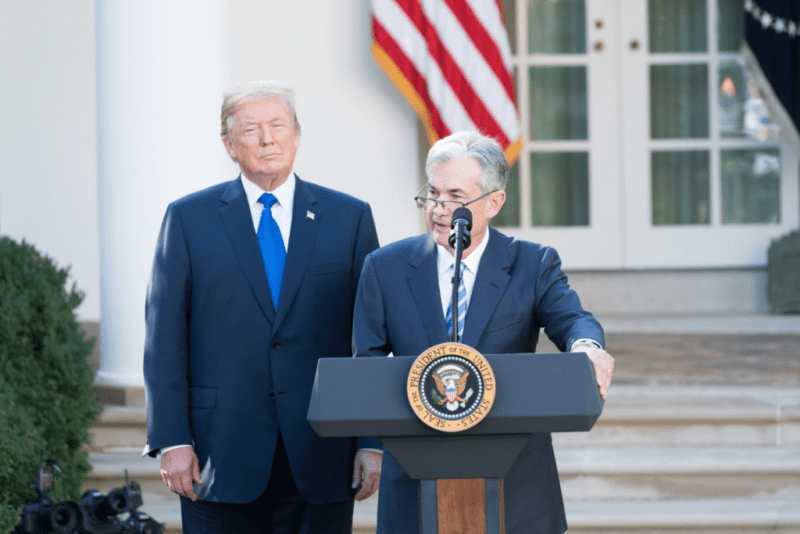

President Trump’s Thursday announcement nominating Kevin Warsh to replace Jerome Powell as Federal Reserve Chairman sent shockwaves through bond markets that had hoped for dovish replacement willing to cut rates aggressively despite persistent inflation, with the selection of a known monetary hawk who served on the Fed Board from 2006 to 2011 signaling that the administration recognizes limits to how far it can push for easier policy without triggering market revolt. Long-term Treasuries underperformed as yields climbed following the announcement, while money markets didn’t react meaningfully with traders slightly increasing bets on two rate cuts during 2026 despite Warsh’s historical advocacy for tighter policy. The nomination arrived as mortgage rates crept higher to average around 6.15% for 30-year fixed loans despite recent Fed cuts, demonstrating how bond market dynamics independent of central bank policy can keep borrowing costs elevated and constrain housing market recovery that depends on affordable financing.

Warsh’s nomination represents Trump’s attempt to thread impossible needle where he selects Fed chair who will support lower rates to boost growth and asset prices while maintaining sufficient hawkish credibility to avoid bond market panic about inflation risks and fiscal sustainability. The former Fed governor has said he supports lower rates, aligning with the president’s preferences, though his previous service during the financial crisis included advocacy for relatively tight policy that prioritized price stability over maximum employment. Senator Thom Tillis, a North Carolina Republican, posted that he would oppose the nomination until the federal criminal probe into Powell is resolved, creating potential confirmation obstacles even though Republicans control the Senate and typically defer to presidential nominees for executive branch positions.

Kathy Jones, chief fixed income strategist at the Schwab Center for Financial Research, noted “Warsh was a hawk in his previous time at the Fed. The question is, will he change his views to please the president?” The central question facing bond investors is whether Warsh would maintain Fed independence and make policy decisions based on economic data and the central bank’s dual mandate, or whether he would capitulate to presidential pressure for easier policy that could reignite inflation and trigger bond market selloff that drives yields substantially higher and creates losses for bondholders.

The 10-year Treasury note yield climbed 2 basis points early Friday following the Fed chair announcement, though market reaction remained muted compared to dramatic moves that typically accompany major monetary policy shifts. The relatively subdued response suggested investors were taking wait-and-see approach, recognizing that Warsh won’t assume the position until May when Powell’s term expires and that substantial uncertainty exists about how the new chairman would actually conduct policy versus his historical positions. The U.S. dollar index climbed slightly after the announcement while gold dropped 4%, though it’s unclear whether these moves reflected direct reaction to Warsh’s nomination or broader market dynamics.

Mortgage rates stepped higher for the week ending January 29 as the Federal Reserve announced a pause from rate cuts and maintained the fed funds rate at 3.5-3.75% following its January 27-28 policy meeting. The disconnect between Fed rate stability and mortgage rate increases demonstrated that residential lending costs depend more on long-term bond yields and mortgage-backed securities pricing than on short-term rates that the Fed directly controls. When 10-year Treasury yields rise due to inflation concerns, deficit worries, or reduced foreign demand for U.S. debt, mortgage rates follow higher regardless of what the Fed does with overnight lending rates.

According to Freddie Mac’s weekly survey, the 30-year fixed mortgage rate averaged approximately 6.15% in late January, representing the lowest level since October 2024 but still more than double the sub-3% rates that prevailed during the pandemic era when the Fed maintained zero interest rate policy and conducted massive quantitative easing purchases of mortgage-backed securities. The current rate environment creates affordability challenges for potential homebuyers who face monthly payments roughly 60% higher than they would have paid for identical homes financed at 3% rates, severely constraining housing demand despite pent-up need from demographic trends and years of underbuilding.

The relationship between Fed policy and mortgage rates has broken down somewhat during the current cycle, with mortgage rates initially moving opposite to Fed rate cuts when the central bank began easing in September 2024. This counterintuitive dynamic reflected bond market concerns that Fed easing would reignite inflation, causing long-term yields to rise even as short-term rates fell. The yield curve dynamics created conditions where the Fed cut rates 75 basis points during late 2024 and early 2025 yet mortgage rates remained relatively stable or even increased slightly, demonstrating that central bank control over borrowing costs has limits when bond markets worry about inflation trajectory or fiscal sustainability.

For personal finance planning, the current environment creates difficult decisions about whether to lock in mortgage rates near 6.15% or wait for potential further declines if the economy weakens and the Fed cuts more aggressively. Borrowers who refinanced during the 2020-2021 period when rates touched all-time lows below 3% have virtually no incentive to refinance at current levels, as the monthly payment savings would be negative and closing costs would never be recovered. However, first-time buyers and those who need to relocate face no choice but to accept current rates or delay purchases indefinitely waiting for unlikely return to pandemic-era financing conditions.

The conventional wisdom that refinancing makes sense when rates fall 2% below current mortgage has become obsolete for the millions who locked in sub-3% rates, as it would require mortgage rates falling below 1% to justify refinancing costs and monthly payment disruption. This dynamic has frozen substantial portion of the housing market as existing homeowners with low-rate mortgages choose to stay put rather than selling and buying replacement homes at 6%+ rates that would dramatically increase housing costs even if the new home’s purchase price remained similar to sale proceeds.

Bond market conditions heading into 2026 suggested solid returns driven primarily by coupon income rather than price appreciation, as Charles Schwab analysts forecast that resilient economic growth and persistent inflation pressures would limit yield declines that drive bond price gains. The yield curve likely will remain steep due to increasing supply in government, municipal, and corporate bonds as federal deficit spending continues, state and local governments finance infrastructure projects, and corporations issue record amounts of debt to fund AI infrastructure buildouts and other capital expenditures.

Treasury Inflation-Protected Securities represent potential opportunity for investors concerned about inflation reacceleration from massive defense spending proposals, tariff-driven import price increases, or wage pressures if labor markets remain tight. TIPS currently offer yields that appear attractive relative to nominal Treasuries if inflation exceeds the roughly 2.3% annual rate implied by breakeven spreads, though investors should recognize that TIPS can underperform dramatically if deflation or disinflation surprises to the downside.

Municipal bonds present compelling opportunities for high-income investors in elevated tax brackets, with tax-equivalent yields on high-quality munis often exceeding 6% for those in the top federal tax bracket once state and local tax benefits are included. However, muni investors must carefully assess credit quality given fiscal challenges facing many state and local governments that struggle with unfunded pension liabilities, declining tax bases in some jurisdictions, and reduced federal aid as Washington grapples with its own deficit problems. The recent financial stresses on some municipalities during the pandemic highlighted that not all municipal debt carries equal safety despite historical tendency to treat munis as low-risk investments.

Corporate bond issuance reached record levels during the first full week of January according to LSEG data cited by BlackRock, with companies rushing to lock in financing before potential market disruptions from Trump administration policies or Federal Reserve decisions. The massive borrowing creates supply that competes with Treasury issuance for investor capital, potentially pushing yields higher across the curve as buyers demand adequate compensation for increased supply. JP Morgan estimates that roughly $300 billion of AI and data center-related debt will be issued during 2026 as hyperscalers and technology companies fund infrastructure buildouts through credit markets rather than equity offerings.

The quality differential between AI-related issuers matters enormously for bondholders, as Microsoft and other hyperscalers with exceptional balance sheets can borrow at rates approaching Treasury yields while speculative data center projects from unproven sponsors must pay substantial premiums to attract buyers. Investors reaching for yield by purchasing lower-quality AI debt should recognize the risks that many data center projects will fail as supply overwhelms demand and that recovery rates on defaulted project debt typically prove disappointing.

High-yield corporate bonds face challenging outlook if economic growth slows or if credit conditions tighten, as the spread between junk bonds and comparable Treasuries has compressed to levels that provide limited compensation for default risk in weakening economic environment. While higher yields remain attractive in absolute terms, the potential for capital losses if spreads widen could offset income advantages and leave investors with negative total returns. Careful security selection and credit analysis become critical in high-yield space where issuer-specific risk dominates sector-wide trends.

The fixed income outlook for 2026 reflects expectations that central bank rate cuts in response to weakening labor markets will drive solid returns, though the bulk of returns will likely come from coupon income rather than price appreciation according to Schwab analysts. Economic growth should remain resilient around 2-2.5% supported by fiscal stimulus from tax cuts and infrastructure spending, keeping inflation near 3% and significantly above the Fed’s 2% target. This environment limits how much the Fed can cut rates without risking inflation reacceleration, potentially disappointing market expectations for aggressive easing.

The “One Big Beautiful Bill Act” fiscal stimulus that Congress passed provides support for economic growth through tax cuts favoring higher-income consumers and corporations, though the legislation also adds to federal deficits that already exceed $1.8 trillion annually before accounting for proposed $600 billion defense spending increase. The mounting debt burden creates longer-term concerns about fiscal sustainability that could eventually trigger bond market revolt if foreign buyers reduce Treasury holdings or if credit rating agencies downgrade U.S. sovereign debt.

Bond investors should consider maintaining intermediate-term duration as strategy to balance price volatility risk from potential yield increases against opportunity to capture attractive coupon income at current levels. Extending too far into long-duration bonds creates substantial price risk if yields rise, while staying exclusively in short-term securities sacrifices yield and requires frequent reinvestment at uncertain future rates. The middle-ground approach of focusing on 5-7 year maturities provides reasonable yield while limiting downside if rates move higher.

The Warsh nomination creates additional uncertainty about future monetary policy direction beyond normal considerations about economic data and inflation trajectory, as investors must assess whether the new Fed chair will maintain institutional independence or cave to presidential pressure for easier policy. Historical precedent suggests that Fed chairs typically prioritize central bank credibility and resist political pressure once in office, recognizing that perceived politicization would damage the institution’s effectiveness and potentially trigger market panic. However, Trump’s unprecedented attacks on Fed independence including DOJ criminal investigation of Powell suggest the administration won’t accept traditional boundaries, creating risks that Warsh faces impossible choice between maintaining independence and keeping his job.

For mortgage borrowers and homebuyers, the slow grind higher in rates despite Fed cuts demonstrates that residential lending costs reflect complex interaction of long-term bond yields, mortgage-backed securities pricing, lender risk assessments, and competitive dynamics rather than simply following short-term policy rates. Prospective borrowers should focus on improving credit scores, maximizing down payments, and comparison shopping across multiple lenders to secure best available rates rather than waiting for dramatic rate declines that may never materialize if bond markets remain concerned about inflation and deficits.